December employment numbers finally popped, and the year turned out to a bit weaker jobs-wise than November had made things appear. Looking at my database activity in January, this does not come as a surprise for me.

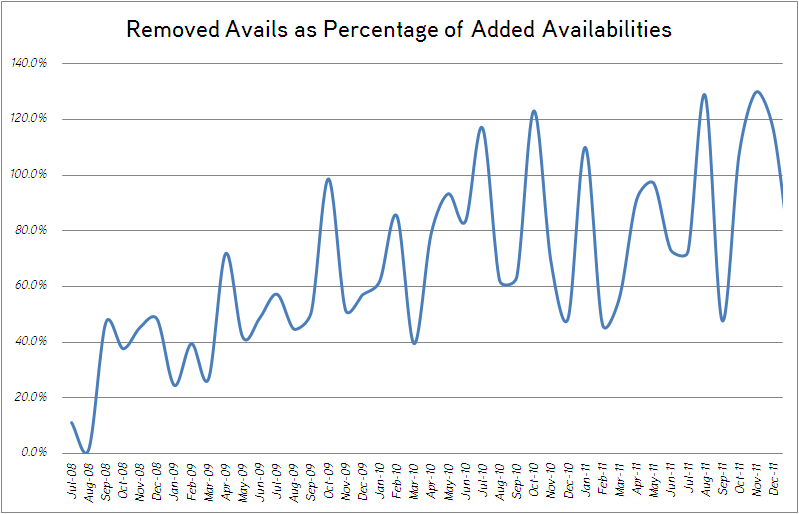

Overall, the trend is still positive, but the climb is so gradual that it isn't hard to miss it. The graph above shows the number of avails removed from the database as a percentage of the number of availabilities added. Now, this is not scientific by any means because it doesn't take into account the size of the leases, but it does give an idea of which direction the market is going. I can say, as they guy who has to enter and remove all of these records, that the trend right now is the new availabilities are bigger than the removed availabilities.

You can see that there have been a few months (July 2010, October 2010, January 2011, September 2011 and November to December 2011) where availabilities removed exceeded availabilities added. Between Jul 2008 and July 2010, there was a pretty steady improvement in this number. Once we hit mid-2010, though, the needled started jumping, so to speak, as though there was an earthquake. Several strong months, several weak months. This is one of factors that is making predicting the next 12 months of the Southern Nevada commercial real estate sector's performance difficult.

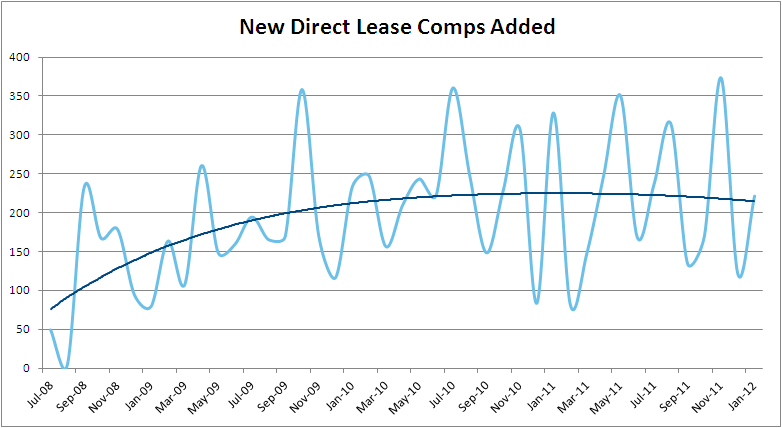

If we drill down a bit, we can see how different types of availability are shaking out.

The number of direct lease comps added to the database showed distinct improvement in 2008/2009. Since then, the trend has flattened out, and January 2012 has bent things in the wrong direction. Perhaps February numbers will change that, but for now, it looks as though leasing activity has "topped out".

The picture is more promising for sales comps. They hid a nadir in early 2009 and have improved since then, but still we see the gaps between "good months" and "bad months" getting very wide in 2011.

What does it all mean? That's the big question. Either things are mellowing out for a month or two before they begin to climb again, or 2011 was our big "recovery" year and 2012 is going to come in a bit weaker. Personally, I believe it is the former rather than the latter, but I'm not counting the latter out.

February will give us a better idea of what lies ahead in 2012. If February is weaker than January, then all bets are off on 2012 being any stronger than 2011 and you can probably flip a coin on whether any given product type posts minimal negative or positive net absorption by year's end.

On the other hand, if February reverses January's course, then it appears that we're in a gradually improving market in 2012. Let's hope for a strong February! Either way, things have grown quite volatile, so keep your seat belt fastened.

No comments:

Post a Comment