After surviving an impressive housing bubble that burst just 5 years ago, many Las Vegans are eying the current housing recovery with a suspicion. The sales figures look good, but with prices increasing by 20% or more year-to-date, are we just entering a new housing bubble?

First, let’s examine the market of yesterday and the market of today. In the period 2005 to 2007, Las Vegas saw an average of 2,625 new homes sell per month, while the median price of a new home increased 5.8 percent over that period. In the past twelve months, new home sales have averaged 573 per month, and the median price of a new home as increased by 11.5 percent. So, obviously, even if a bubble is forming now, there is a magnitude of difference in scale between what was occurring then and what is occurring now.

The activity of investors is often pointed to as another similarity between then and now, but this is not quite so. The investors that caused heartache a few years ago were often over-leveraging themselves to buy homes that they thought they could re-sell at a tidy profit in just a few months. Unfortunately, they discovered that the amazing price increases they were seeing were all due to the activity of other investors, and even with very low interest rates and the willingness of traditional home buyers (or lack of knowledge) to borrow far more than they could afford, the investors priced the occupiers of homes out of the market, found they could not keep up their mortgage payments, and the market collapsed. Home builders, working feverishly to keep up with the perceived demand, built many more houses than were needed, and thus the housing crisis and the Great Recession.

How are things different today? The investors of today are not the investors of yesterday. Having spoken to people within the housing industry in Southern Nevada, I have found that the individual investors of today are coming in with plenty of cash and are not over-leveraging themselves to buy investment homes. Moreover, many of the investment sales we are seeing in Southern Nevada today are by institutional investors, buying hundreds of units, often directly from banks.

How are things the same? When housing sales are driven by investors, they leave a gap in the market. From the perspective of home builders, a house sold is a house that is off the market. In fact, though, an empty house is still effectively on the market. When tracking commercial real estate, vacancy is the thing that matters! An investment property must eventually pay for itself, either by means of rent paid by an occupant, or by the value of the property appreciating past the value of the loan taken out to buy the property in the first place. The last bubble was driven by such appreciation of value, not by renters occupying houses, but the appreciation could not keep pace with the prices being paid for houses.

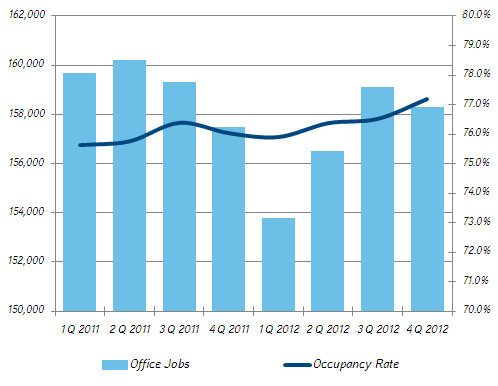

More importantly, when home builders saw houses selling a few years back, they took it as a sign that more houses were needed. Home builders today are gearing up to begin building houses in earnest once again in 2014. The question is whether they are building for investors or for occupants? Unfortunately, the vacancy rate for single-family homes is notoriously hard to determine, with different groups (the U.S. Census Bureau being one) coming up with wildly different numbers. This is unfortunate, because it would fill a crucial gap in our knowledge of the home market.

One clue to whether Southern Nevada is once again getting ahead of itself might be found by comparing household growth in Clark County (based on information from the Clark County Demographer and Claritas) to new home sales (based on information from Dennis Smith’s Home Builders Research). Demographic data from Claritas states that 42.9 percent of households in Clark County rent homes or apartments rather than own single family homes or condos, so we’ll adjust the household growth figures by 43 percent to get a better idea of how many buyers were entering Clark County each year.

What does this graph tell us? First and foremost, in-migration into Southern Nevada dropped sharply in 2008, 2009 and 2011, but has generally been on the rebound in the past two years. Second, we see that new home sales decreased substantially in 2007, at the beginning of the housing crisis, and continued to plummet in 2008 and 2009; in 2012 they began a slow recovery.

In 2005 and 2006, Southern Nevada was selling approximately three times as many new homes as it was adding new households that were likely to own homes. This suggests that most of these new homes were purchased by investors rather than occupants. The percentage declined in 2007, reaching what would be the lowest percentage in the nine years covered by this chart. In 2008, the first full year of the Great Recession, almost five times as many new homes were sold as new households moved into Southern Nevada, despite a steep decrease in the number of new homes sold. Since 2009, Southern Nevada has gained an average of 1,300 households per year and sold an average of 5,400 new homes per year, again, more than 4 times as many new home sales as new households likely to own rather than rent entering the region.

In 2013, Clark County is projected to expand by 3,200 households and sales, if they remain steady, should reach 7,200 new homes, approximately a 2:1 ratio. While this is not as high a ratio of new home sales to new households as recorded in 2005, 2006 and 2008, it is higher than in 2007 (when the market began to cool), 2010 (when the federal government juiced the housing market) and 2012. This suggests that investors once again are beginning to dominate the housing market. Fortunately, they are buying new homes at lower prices (28 percent lower) than they were in 2005, but the median price of a new home has increased by 13 percent in the past five months. While this is good for house flippers (though we know how that story ends), it is bad for owner/users and problematic for landlords, as they must still compete with multi-family projects and cheaper, existing homes that are on the rental market.

If Southern Nevada’s population was expanding more rapidly, and if the median new home price was expanding much more slowly, I would feel more comfortable about the current expansion in new home sales. As it stands, home builders must be very careful about new home construction in 2014, as they might once again find themselves building more homes than they can sell if investors once again cool on Southern Nevada.

{kind=link}